FHA Mortgage Insurance

FHA loans are extremely popular with more than 25% of all mortgages being FHA insured. Home buyers with a very small down payment or lower credit scores are able to finance their dream homes using an FHA home loan.

With the benefits of qualifying with a low-down payment comes the added expense of the FHA mortgage insurance as part of your FHA closing costs. Learn about FHA mortgage insurance and how much it will cost before you move forward with your mortgage.

What is FHA Mortgage Insurance?

The FHA Mortgage Insurance Premium (MIP), is the FHA’s version of PMI. It is an additional fee paid by the borrower to protect the lender from losses in the event the loan defaults. There is an upfront insurance premium of 1.75% of the loan amount at closing, and then a monthly premium for the life of the loan.

Get a Mortgage Quote Here and find out how much the mortgage Insurance will be.

How Long is FHA Mortgage Insurance Required?

FHA mortgage insurance is required for the life of the loan. However, with a down payment of 10% or more, the FHA mortgage insurance can be removed after 11 years. You have the option of selling the home or refinancing out of an FHA loan to have the FHA mortgage insurance removed.

How Much is FHA Mortgage Insurance?

On average, FHA mortgage insurance will cost about $.70 for each $1000 of loan amount. In this example, if your loan amount is $200k, your monthly FHA mortgage insurance payment would be about $140.

How is FHA Mortgage Insurance Calculated in 2024?

There are two components to FHA mortgage insurance. The portion first is the upfront mortgage insurance premium of 1.75% of the loan amount.

As an example, if your purchase price is $243,500 and your loan amount is $235,000, then your upfront mortgage insurance premium at closing will be $4,112.50 ($235,000 X 1.75%)

The upfront mortgage insurance premium needs to be paid on all FHA loans except the following:

- FHA Streamline Refinances

- Loans on Indian lands

- Loans on Hawaii Home Lands

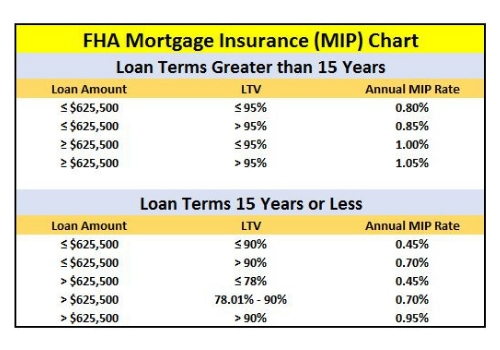

The second portion is the annual FHA mortgage insurance premium which is divided by 12 and added to your monthly mortgage payment. The calculation of this payment will vary based upon the loan amount and your down payment amount or loan to value ratio (LTV).

Example: Loan amount of $235,000 + 96.5% LTV + 30 yr fixed loan

- $235,000 X .85% = $1,997.50

- $1,997.50 Divided by 12 = $166.46

- $166.46 is added to your monthly mortgage payment

You can see from the chart below, the loan amount is less than $625,000, the LTV is greater than 95% and the mortgage term is greater than 15 yrs. So, the rate used for the MIP calculation is .85%

Total FHA Mortgage Insurance Premium in the example above = $4,112.50 plus $166.46 per month

Tip – the more money you put down on the home, the lower your MIP rate will be that is used to calculate your monthly insurance premium. This could save you a lot of money over the life of your loan

Update – Effective March 2024, the mortgage insurance premium has been reduced by .30%

FHA Mortgage Insurance Calculation Chart

This chart is the guide you should use when determining the annual mortgage insurance premium for your loan. Most individuals who are considering an FHA loan will likely fall into the less than $625,500 loan amount category and with a term greater than 15 years.

FHA Upfront MIP (mortgage insurance premium)

The FHA upfront MIP is equal to 1.75% of the loan amount and must be paid at closing. If your loan amount is $200,000 for example, the FHA upfront MIP will be $3,500.

The FHA upfront MIP must be paid at closing and can be funded in the following ways:

- Cash at closing from the borrower

- Included in the total loan amount

- Gift funds from a relative or close friend

- Funded by the seller as a closing cost credit

- Funded by the lender as a lender credit.

Keep in mind that if he lender covers the FHA upfront MIP for you, the rate will likely be slightly higher. There is no way to avoid having an FHA upfront MIP fee on your FHA loan because it is required per the FHA guidelines.

Can the FHA Up Front Mortgage Insurance (MIP) Fee Be Financed?

The upfront FHA mortgage insurance fee can be financed or rolled into the loan. This a huge benefit for those who don’t have very much saved for closing costs. Here are some of the features or rules around financing the FHA up front mortgage insurance fee:

- The fee must be paid in cash or financed

- The fee cannot be split by financing some of it and paying cash for the rest. It is one or the other

- Financing the fee does not impact your DTI or reduce the loan amount that you qualify for.

- The upfront fee is not considered to be part of the minimum down payment amount

Financing the FHA up front mortgage insurance fee means you will be paying interest on it for the life of the loan.

Tip – negotiate with the sellers of the home to have them cover this cost at closing. This is considered to be a seller concession.

Can the Upfront FHA Mortgage Insurance be Gifted?

The upfront FHA mortgage insurance can be gifted by a relative or close friend per the FHA Guidelines. The FHA gift funds could cover the down payment plus some or all of the FHA closing costs. When you find yourself short on cash to purchase the home, then a gift may be what you need.

How to Remove Mortgage Insurance (MIP) from an FHA Loan

If you were assigned your FHA case number on or before June 3rd, 2013 AND your loan balance is now at or below a 78% loan to value, you can request to have the annual/monthly mortgage insurance premium dropped.

If your FHA loan is dated after June 3rd 2013 and you put more than 10% down, you can request to have the FHA mortgage insurance (MIP) removed after 11 years. Important to note is the waiting period is a minimum of 11 years so even if you pay down your loan faster and reach 78% LTV, you still need to wait 11 years.

If your FHA loan is dated after June 3rd 2013 and you put 10% or less down, then the FHA mortgage insurance premium is in effect for the life of the loan and cannot be cancelled. In this scenario, the only possible way to free yourself from the FHA mortgage insurance premium is to refinance to a loan program that is not FHA insured, or sell the home.

FHA Mortgage insurance vs PMI for Conventional Loans

There are a few significant differences between FHA mortgage insurance premiums (MIP) and PMI for conventional loans. Conventional PMI is calculated using the loan amount, credit score and LTV as the main factors in determining your monthly PMI payment. Here are some other things to know:

PMI can be cancelled or removed if you pay the balance down below 80% of the original appraised value. If you forget, the lender is required to do it automatically once it reaches 78%.

The PMI monthly insurance payment will likely be more than FHA mortgage insurance (MIP), but it is not enforced for the life of the loan.

In our example above with the $243,500 purchase and $235,000 loan amount, the monthly PMI payment for a conventional loan would be $236.96 versus $166.46 for the FHA mortgage insurance. We used the MGIC calculator to determine the PMI payment.

How to cancel FHA Mortgage Insurance

If your FHA loan is dated after July 3rd, 2013 you cannot cancel it unless your original down payment was greater than 10%. If your down payment was greater than 10%, you can cancel the FHA mortgage insurance once the loan balance drops to a 78% LTV.

Summary – FHA Mortgage Insurance

Most home buyers save for a down payment, but FHA mortgage insurance is something that is often overlooked when determining the costs to purchase a home. By now you should be fully educated on the FHA mortgage insurance component of your real estate transaction. Plan ahead and determine how you will cover these costs.

Related Questions

Does FHA have PMI?

FHA loans have their own version of PMI called MI and it is mandatory on every FHA loan.

Is FHA Mortgage Insurance Tax Deductible?

The FHA mortgage insurance premium may be tax deductible if your adjusted gross income does not exceed $109,000 per year. It is important to note we are not monitoring the changes in the tax laws closely and this figure may not be up to date. You should consult an accountant for tax planning purposes.

Is FHA Mortgage Insurance Considered to Be Part of Closing Costs?

One of the most common home buyer mistakes is not setting enough money aside for all of the costs related to the purchase of the home. The FHA upfront mortgage insurance premium is possibly the single largest closing cost item that you may have outside of your tax escrows.

Why did my FHA Mortgage Insurance Go Up?

If you already have an FHA loan, the FHA mortgage insurance should never increase. At one time, the FHA changed how the upfront mortgage insurance premium and the annual insurance premium were calculated. They increased the annual amount but only for future loans, not existing loans.

Does FHA Mortgage Insurance Cover Death?

The FHA mortgage insurance is not a death benefit insurance policy. It is there to protect the lender in the even of default. If the homeowner passes away and the mortgage cannot be paid, the FHA mortgage insurance would refund the lender for any losses they incur after a foreclosure.

Related Articles

FHA Mortgage Insurance and High Risk Lending